Tax Code 1257L M1 Explained: What It Means for Your Pay in 2026/27

Tax code 1257L M1 explained for 2026/27, including emergency tax, monthly allowances, payslip examples and how to fix it.

Tax Code 1257L M1 Explained: What It Means for Your Pay in 2026/27

If tax code 1257L M1 has appeared on your July 2026 payslip, do not assume your employer has made a mistake. It is an emergency, or non-cumulative, version of the standard code. You still receive a tax-free allowance for the month, but payroll ignores pay and tax from earlier months when it works out this payday’s Income Tax.

That can be perfectly sensible when you have just started a job and HMRC does not yet have the full picture. It can also leave you paying too much, or occasionally too little, tax for a while. The important bit is understanding what the letters and numbers mean, then checking whether HMRC has the right information.

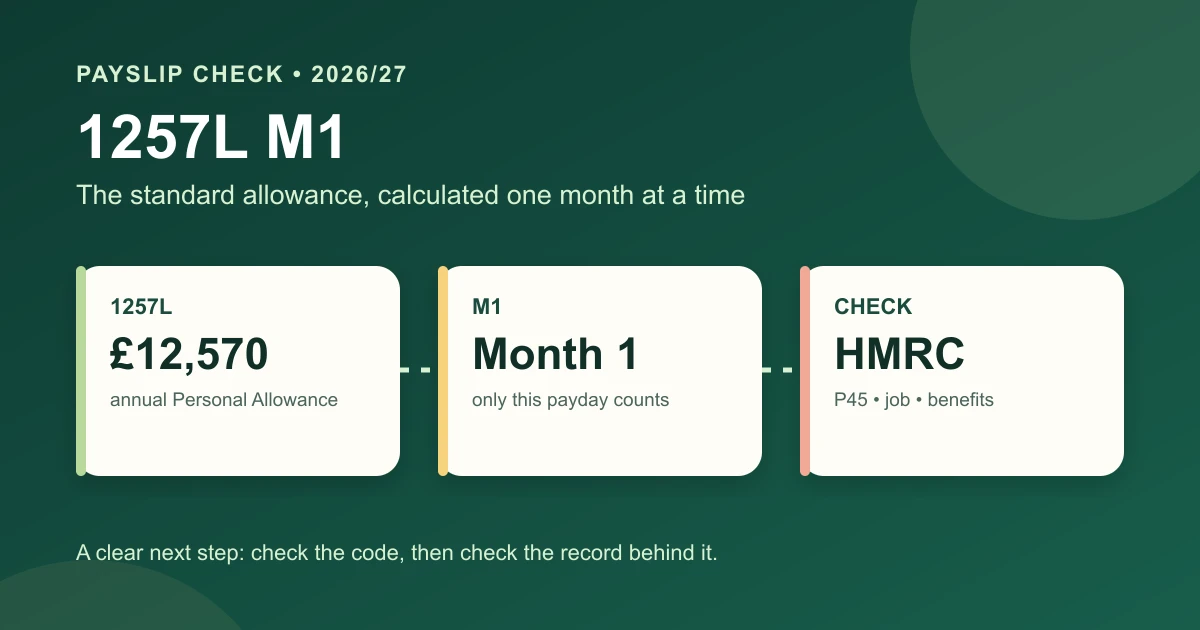

Quick answer: for 2026/27, 1257L represents the standard £12,570 Personal Allowance. M1 means month 1, so your employer treats each monthly payday on its own instead of using your total pay and tax since 6 April. The similar codes W1, X and NONCUM work on the same non-cumulative principle.

We often see tax-code questions alongside payroll setup, a job change, or a director starting to take a salary. Our payroll service, bookkeeping support, and contact page can help if the records behind the code need sorting out.

What tax code 1257L M1 means in 2026/27

Start with the numbers. HMRC uses the number part of a tax code to tell an employer roughly how much tax-free income to give you in that job or pension. Add a zero to 1257 and you get £12,570, the standard Personal Allowance for the tax year running from 6 April 2026 to 5 April 2027.

The L normally means you are entitled to the standard Personal Allowance. It is the normal code for someone with one job or pension and no adjustment for things such as taxable benefits, unpaid tax from an earlier year, or a second source of income.

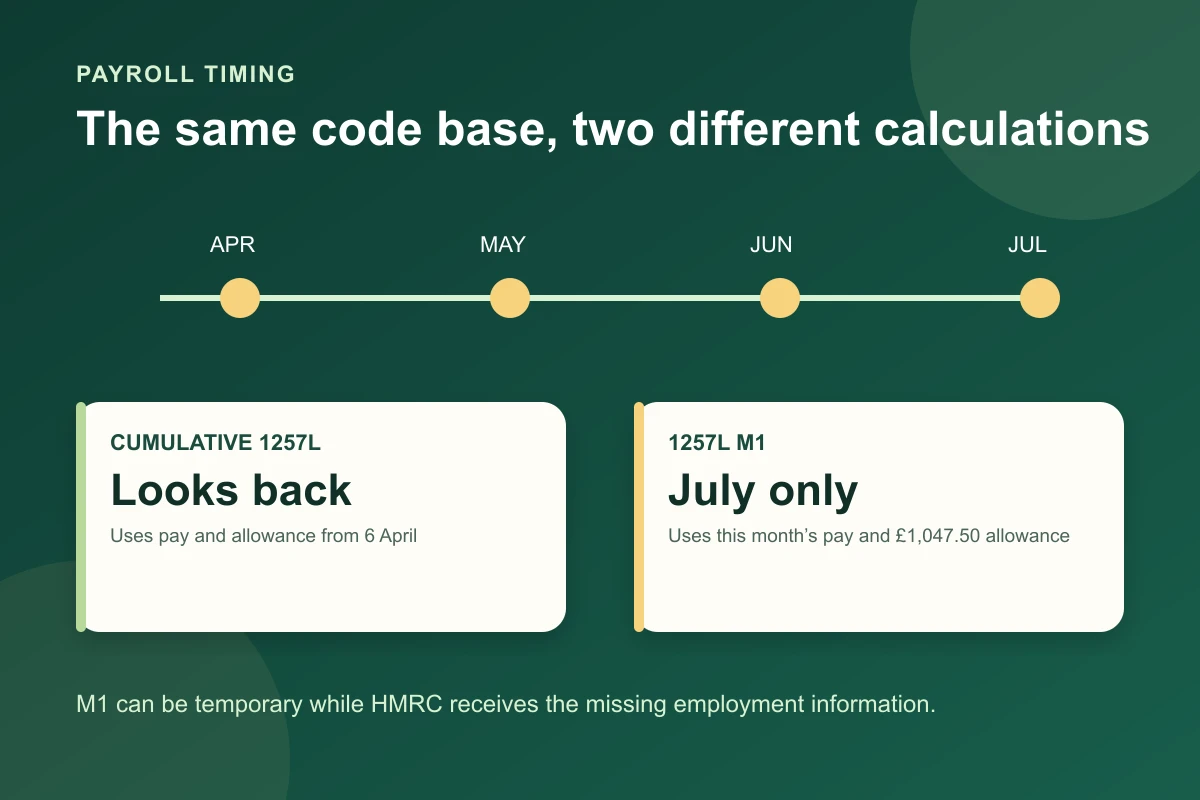

The M1 is the part people miss. It means month 1. Your monthly payroll uses one twelfth of the annual allowance, which is £1,047.50, and applies the tax bands to that pay period only. It does not look back to April, May or June and correct the running total.

For most employees in England, Wales and Northern Ireland, the relevant 2026/27 figures are:

| Item | 2026/27 figure | Why it matters on 1257L M1 |

|---|---|---|

| Standard Personal Allowance | £12,570 a year | The number behind 1257L |

| Monthly allowance | £1,047.50 | Used for each monthly M1 payroll calculation |

| Basic-rate band after allowance | £37,700 a year | The annual band behind the usual 20% rate |

| Standard basic Income Tax rate | 20% | Often the first rate used after the monthly allowance |

| Higher-rate threshold with standard allowance | £50,270 a year | Relevant if your monthly income is high enough |

Scotland has its own Income Tax bands and a Scottish prefix, such as S1257L M1. Wales may use a C prefix. The M1 logic is still about the payroll period, but the rates and bands can differ. It is worth checking your code rather than assuming a colleague’s payslip tells you the answer.

Is 1257L M1 an emergency tax code?

Yes. GOV.UK treats a code ending M1, W1, X or NONCUM as an emergency tax code. The word sounds dramatic, but it usually means payroll is waiting for information, not that HMRC thinks you have done anything wrong.

You may see it when:

- you have started a new job and did not give your employer a P45

- your new employer has not yet received HMRC’s tax-code notice

- you have moved from self-employment into PAYE work

- you have started drawing a pension while still working

- the payroll team needs a temporary code while HMRC checks a change in income, benefits or employment

In a cumulative tax code, payroll considers your allowance and tax paid from the beginning of the tax year. That often corrects a small overpayment or underpayment automatically later in the year. An M1 code deliberately does not do that. It gives you a clean monthly calculation until HMRC sends a cumulative code or the employer has the records needed to use one.

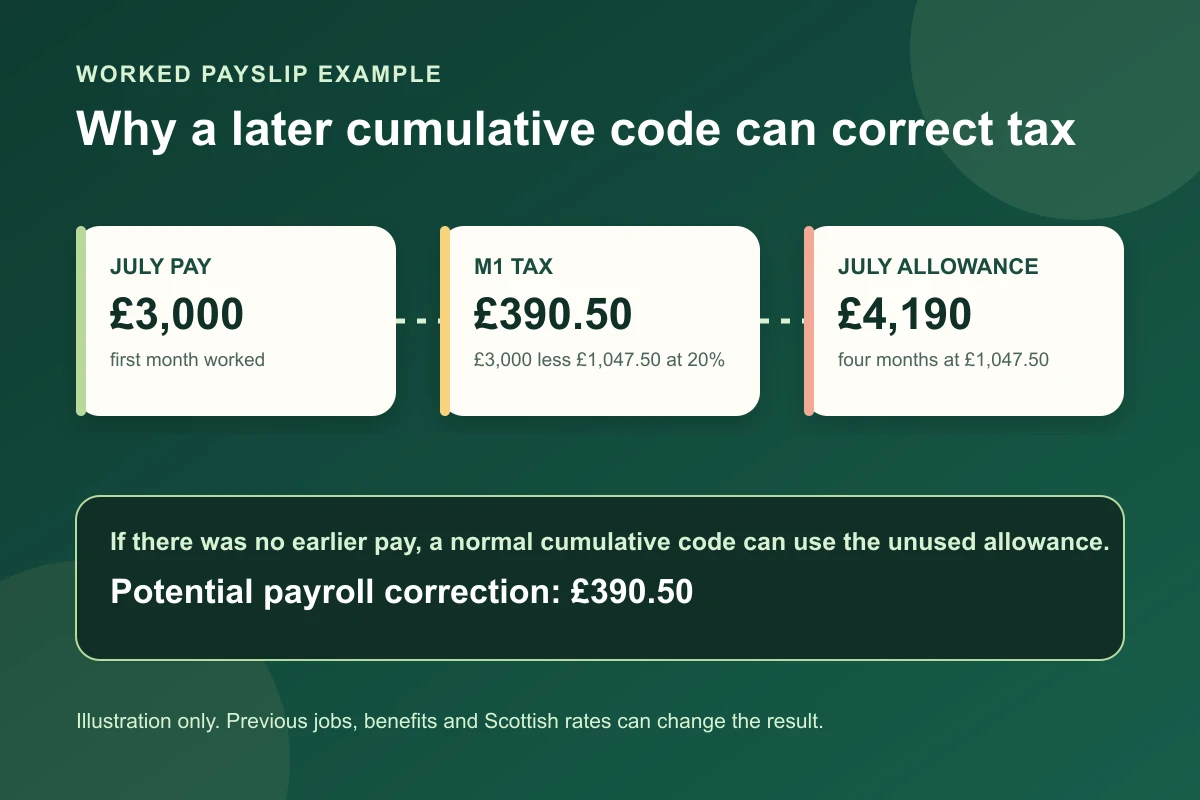

Worked example: 1257L M1 on a £3,000 monthly salary

Assume Priya starts a new job in July 2026 on £3,000 a month. She has no P45 ready for payroll, so her first payslip uses 1257L M1. Ignore National Insurance, pension deductions and student loans for this simple Income Tax example.

| Step | Calculation | Amount |

|---|---|---|

| Monthly gross pay | £3,000.00 | |

| Monthly Personal Allowance | £12,570 ÷ 12 | £1,047.50 |

| Taxable pay for the month | £3,000.00 less £1,047.50 | £1,952.50 |

| Basic-rate Income Tax | £1,952.50 × 20% | £390.50 |

Her July Income Tax is £390.50 under the straightforward M1 calculation. The code has not taken April to June into account. If Priya had no earnings in those earlier months, a later cumulative calculation may give her more unused allowance and change the year-to-date tax position.

The exact answer changes with benefits, a second job, Scottish rates, salary sacrifice, taxable interest collected through PAYE, and other adjustments. Still, this example shows why M1 is not the same as being taxed at a special emergency rate. The rate can still be the ordinary 20% basic rate. The difference is the period used to calculate it.

Why an M1 code can make your tax look wrong

The tax code is not automatically wrong. The temporary calculation may be the best payroll can do with the information it has. Trouble starts when it stays in place after the missing records have caught up, or when HMRC’s estimated income is not right.

Here is a common pattern. Daniel left a job at the end of May after earning £8,000 in the tax year. He starts a new job in July on £3,000 a month and is put on 1257L M1. The July payroll gives him only July’s £1,047.50 allowance, even though the cumulative allowance available by the end of July would be £4,190. His former employer’s P45 and HMRC record decide how the final year-to-date calculation should work, not a rough comparison with one monthly payslip.

The opposite can happen too. If you have already used most of your allowance in an earlier job, a temporary month-one code can look generous on one payday. When HMRC combines the income records, later tax deductions may rise to put the overall year right.

That is why we would not recommend trying to fix the position by asking an employer to invent a different code. Employers should use the P45, starter declaration and HMRC coding notices. You should check the information HMRC holds and correct the underlying facts.

1257L M1, 1257L W1 and 1257L X: the practical difference

The suffix tells payroll which pay period to treat on its own.

| Code ending | Usually seen with | What it means |

|---|---|---|

| M1 | Monthly pay | Month 1 basis. Only the current month’s pay is used. |

| W1 | Weekly pay | Week 1 basis. Only the current week’s pay is used. |

| X | Variable pay dates | Non-cumulative basis where pay dates vary. |

| NONCUM | Some payroll systems | Another way of showing a non-cumulative calculation. |

| No suffix, for example 1257L | Normal payroll | Cumulative calculation from the start of the tax year. |

The number and L can remain the same across those codes. The important distinction is not a different annual allowance. It is whether payroll has permission to revisit earlier pay periods as the year progresses.

Worked example: why the cumulative code may later refund tax

Take Priya again. She did not work from 6 April to 30 June, then earns £3,000 in July. Her M1 payslip uses one month of allowance, £1,047.50, leaving £1,952.50 taxable at 20%, or £390.50 tax.

If HMRC later issues a normal cumulative 1257L code for July, the cumulative allowance by month four is £4,190. Her total pay to date is only £3,000, so in this stripped-back example there is no taxable income left after the available allowance. Payroll could then refund the £390.50 already deducted through a later payslip.

Real payroll is rarely that neat. A previous job, benefits, a different code, pension income, bonus pay or Scottish tax rates may change the result. The useful lesson is that a refund can be automatic once the correct cumulative code reaches payroll. There is no need to wait for the following January if HMRC corrects the record during the tax year.

What to do if you think 1257L M1 is wrong

Do the easy checks first. Find the tax code on your latest payslip and compare the employer name, pay figure and tax paid with your own records. Then sign in to HMRC’s Check your Income Tax service. It covers the current 2026/27 tax year and lets you see the code, Personal Allowance, estimated job and pension income, and changes HMRC has recorded.

Next, check whether one of these actions is needed:

- give your employer your P45 if you have one and payroll has not received it

- complete the starter declaration accurately if you do not have a P45

- update HMRC if you have started or stopped a job, begun a pension, or your estimated pay is wrong

- check whether a company car, medical insurance or other benefit has reduced your allowance

- tell HMRC about a second job instead of assuming both jobs can use a full allowance

- wait for the next payslip after HMRC issues a revised code, then check whether payroll has applied it

For an employer, the control is simple but important: use the authorised tax code in the payroll notice, keep starter records, and do not use an employee’s verbal guess in place of a P45 or HMRC instruction. Our payroll team can review a payroll handover where several starters, benefits or director changes have arrived at once.

Other codes that should prompt a closer look

1257L M1 is common, but it is not the only code that can surprise people.

| Code | General meaning | Useful next step |

|---|---|---|

| 0T | No Personal Allowance is being given | Check whether HMRC needs information about another job or missing details. |

| BR | All pay from that job is taxed at basic rate | Often used for a second job or pension. Check it matches your income setup. |

| D0 | All pay from that job is taxed at higher rate | Check whether it is a second source of income or an estimated-code adjustment. |

| K code | Deductions exceed the available Personal Allowance | Check the notice closely, especially benefits and prior-year tax. |

| S prefix | Scottish Income Tax rates apply | Confirm your main home address is correct with HMRC. |

| C prefix | Welsh Income Tax rates apply | Confirm your main home address is correct with HMRC. |

Do not panic if you see one of these. A code is an instruction for collecting Income Tax through PAYE, not a final verdict on your whole tax position. The GOV.UK tax-code guide explains the letters, while HMRC’s online account is the better place to check the figures attached to your own record.

A quick payslip checklist before payday becomes a bigger problem

Use this short check when a new tax code appears:

- write down the exact code, including M1, W1, X or NONCUM

- check whether you have a P45 from your previous job

- compare your employer and pension details with HMRC’s online account

- check whether HMRC’s estimated annual pay is sensible

- look for taxable benefits, a second job or a pension that could explain an adjustment

- keep the payslip that first showed the code and the next one after any correction

- ask for help if the code or year-to-date figures still do not match the records

One clean check now is usually easier than untangling a run of payslips later. If you run a small business and a new starter’s tax code does not make sense, give payroll the P45 or starter information promptly and let HMRC’s notice do the rest.

Tax code 1257L M1 FAQs

Does 1257L M1 mean I am paying emergency tax?

Yes. M1 means payroll calculates tax using only the current monthly pay period. It does not automatically mean the tax rate is higher than normal, but it can make the amount on one payslip differ from a cumulative calculation.

Will HMRC refund tax deducted under 1257L M1?

If HMRC issues a cumulative code and your year-to-date record shows too much tax was deducted, payroll can normally correct it through a later payslip. The result depends on all your pay, benefits and tax records for the year.

Is 1257L the standard tax code for 2026/27?

Yes. The basic Personal Allowance remains £12,570 for 2026/27, so 1257L remains the emergency code base for employees entitled to the standard allowance. The M1 suffix is what makes it a month-one emergency code.

How do I get off an M1 tax code?

Give your employer a P45 if available, complete the starter declaration accurately, and check your employment details in your HMRC Personal Tax Account. HMRC can send the employer an updated code when its records are complete.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

Employment Allowance UK 2026/27: Who Can Claim, Who Cannot, and How to Apply

Employment Allowance UK 2026/27 explained, with who can claim, who cannot, EPS steps, and worked examples for small employers.

How to Run Payroll for the First Time in the UK: New Employer Checklist for 2026

Learn how to run payroll for the first time in the UK, from HMRC registration and pensions to PAYE deadlines, costs, and first payday checks.

PAYE Deadline 22 May 2026: What Happens If You Pay HMRC Late?

PAYE deadline 22 May 2026 explained for UK employers, with late payment penalties, interest, Time to Pay options, and worked examples.