P46 Car Form Deadline 2026/27: Company Car Reporting Guide

P46 Car form deadline 2026/27 explained for employers, with quarterly dates, payroll rules, company car tax examples, and checks.

P46 Car Form Deadline 2026/27: Company Car Reporting Guide

The P46 Car form deadline is easy to miss because it does not feel as loud as the P11D deadline. A director gets a new company car, an employee gives one back, a fuel card starts being used privately, or payroll starts payrolling car benefits. Nobody panics in the moment. Then, months later, HMRC’s tax code, payroll record, P11D, and Class 1A National Insurance figures do not line up.

For the 2026/27 tax year, employers need to know when a P46(Car) is still needed, when the company car details should go through payroll instead, and how the quarterly reporting dates work. The first key date in the current cycle is 5 July 2026, because that is the end of the quarter for car changes from 6 April to 5 July 2026. The electronic filing deadline for that quarter is 2 August 2026.

Quick summary: use P46(Car) to tell HMRC when an employee or director first gets a company car, stops having one, or has fuel for private use added or removed, unless the car benefit is correctly payrolled. For 2026/27, quarterly electronic deadlines include 2 August 2026, 2 November 2026, 2 February 2027, and 5 April 2027 for the final quarter. Car benefit calculations still feed year-end Class 1A National Insurance, even where tax is collected through payroll.

If company cars sit between payroll, bookkeeping, and director decisions in your business, get the records joined up early. We can help through our payroll services, bookkeeping service, or a direct conversation through our contact page.

P46 Car form deadline 2026/27: the dates employers need

HMRC splits P46(Car) reporting into quarters. The date you use depends on when the company car or private fuel position changed.

The rules are not hard, but the names are unhelpful. The form is called P46(Car), not the old employee starter form P46. It is specifically about company cars and car fuel, not general payroll setup.

For employers filing online, the main 2026/27 dates are:

| Car change period | Online P46(Car) deadline | Paper P46(Car) deadline |

|---|---|---|

| 6 January to 5 April 2026 | 5 April 2026 | 3 May 2026 |

| 6 April to 5 July 2026 | 2 August 2026 | 2 August 2026 |

| 6 July to 5 October 2026 | 2 November 2026 | 2 November 2026 |

| 6 October 2026 to 5 January 2027 | 2 February 2027 | 2 February 2027 |

Those dates come from HMRC’s reporting company car changes guidance. The final quarter is the odd one because the online date is 5 April, while the printed form date is 3 May.

Right, so the deadline is not always the same as the date the car changes hands. If an employee receives a company car on 10 June 2026, the change falls in the 6 April to 5 July quarter. The online deadline is 2 August 2026. If the car starts on 10 August 2026, the deadline moves to 2 November 2026.

The practical problem is that the person who orders the car is not always the person who runs payroll. A director signs the lease, the vehicle arrives, insurance is arranged, and payroll may only hear about it when an employee asks why their tax code changed. That is how avoidable errors start.

When do you need to send a P46(Car)?

You normally use P46(Car) when an employee or director has a company car available for private use and HMRC needs to know about the change during the tax year.

Common triggers include:

- a company car is first made available to an employee or director

- a company car stops being available

- the employer starts providing fuel for private use

- private fuel is withdrawn

- the car details change, such as a replacement vehicle

- a payroll error means the car data has not been reported in the right route

The point of the form is timing. Without an in-year report, HMRC may not adjust the employee’s tax code until much later. That can leave the employee underpaying tax during the year, then facing a catch-up bill through Self Assessment or a later tax code.

If the car benefit is taxed through payroll, you may not need to send a separate P46(Car) in the same way. HMRC says employers who payroll taxable company car benefits must send car data through the Full Payment Submission, usually called the FPS. That is the same Real Time Information submission used for payroll.

The key phrase is “correctly payrolled”. If payroll is not set up to report the car details properly, the business should not assume HMRC has all the data. A car can be taxed monthly, but still be wrong if the list price, CO2 emissions, available dates, or fuel details are wrong.

Our earlier guide to payrolling benefits in kind explains the wider move from P11D reporting to payroll collection. Treat company cars as the fiddly version of that rule, because the calculation changes when the car, fuel, dates, or employee contributions change.

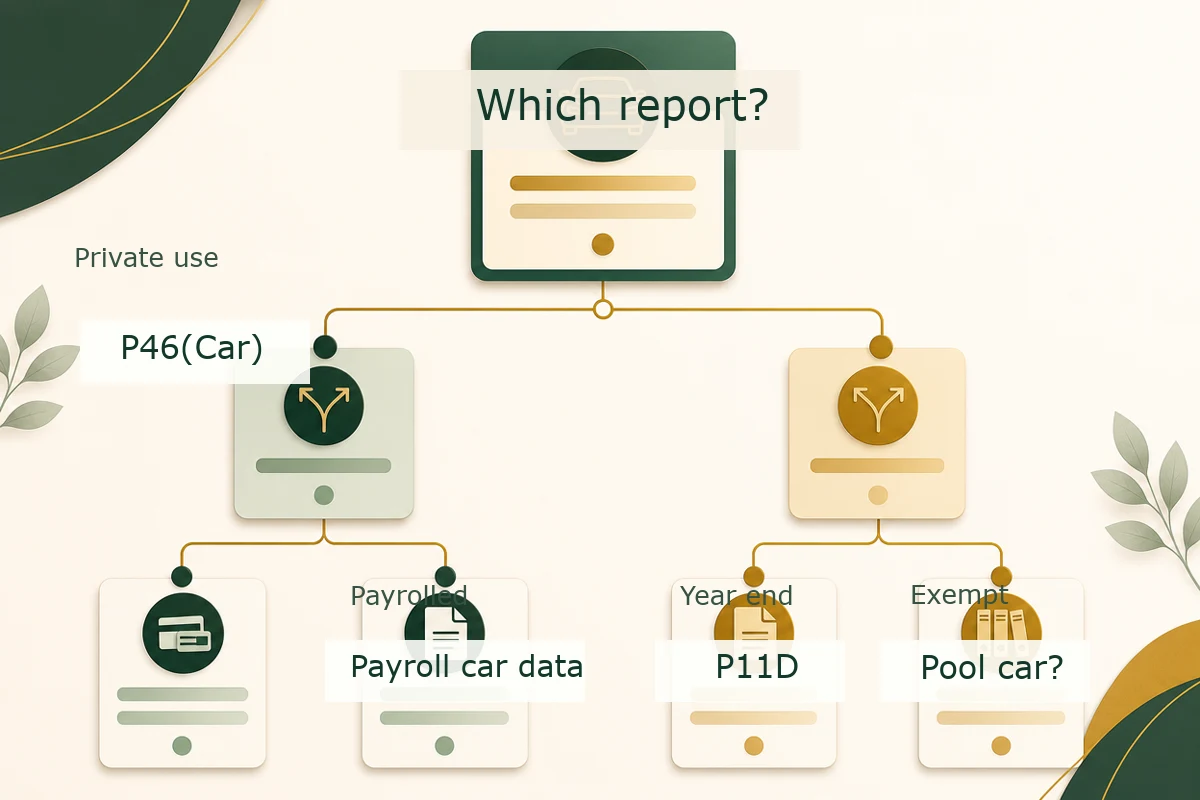

P46(Car), payroll, or P11D: which route applies?

There are three separate jobs that often get mixed together.

| Route | What it does | When it matters |

|---|---|---|

| P46(Car) | Tells HMRC about an in-year company car or fuel change | Needed where car data is not being reported through payroll |

| Payroll car data | Taxes the car benefit through payroll and sends car details on FPS | Used where the employer has registered and set up payrolling correctly |

| P11D | Reports taxable benefits after the tax year where they were not payrolled | Still relevant for non-payrolled benefits and some year-end positions |

| P11D(b) | Reports employer Class 1A National Insurance on benefits | Usually still needed, including for many payrolled benefits |

That last line catches employers out. Payrolling the employee’s tax does not remove the employer’s Class 1A National Insurance job. The Class 1A figure is reported after the tax year on P11D(b). For the 2025/26 benefits cycle, the P11D and P11D(b) deadline is 6 July 2026, with electronic Class 1A NIC payment due by 22 July 2026.

If your current issue is year-end benefits reporting rather than in-year car changes, read our P11D deadline 6 July 2026 guide. This P46(Car) guide is about the car change process that happens before the year-end form.

The thing is, one car can touch all three areas. A car starts in June, HMRC needs in-year data. Payroll needs the monthly taxable benefit if the car is payrolled. At year end, the employer still needs the Class 1A NIC position. Missing one part can make the other two look odd.

What information do you need before reporting a company car?

Do not start with the form. Start with the records. A company car tax calculation is only as good as the details behind it.

For each car, keep:

- employee or director name and National Insurance number

- car make, model, registration, and date first registered

- date the car was first available and date it stopped being available

- list price, including standard accessories

- accessories added later, where relevant

- CO2 emissions figure

- fuel type

- electric range for some hybrid cars

- any capital contribution made by the employee

- any private use contribution paid by the employee

- whether private fuel was provided and the dates it started or stopped

Some of those details live in the vehicle order, some in the lease documents, some in payroll, and some in the bank feed. That is why bookkeeping matters here. If private fuel reimbursement is posted to a vague motor expenses code, it may not get picked up until too late.

There is also a policy decision. Who is allowed private use? Are employees allowed a fuel card? Must they reimburse all private fuel? Is the car payrolled? A small company with two directors and one employee can still make a mess if nobody writes the policy down.

Worth mentioning though: not every business vehicle creates a company car benefit. Proper pool cars can be exempt if the conditions are met. Vans have separate rules. Business-only use can change the answer, but ordinary commuting is usually private use for tax purposes. Do not label something a pool car just because more than one person has driven it.

How company car tax is calculated

Company car tax is based on the car’s taxable benefit value, not on the monthly lease payment. The broad calculation is:

| Step | What you check |

|---|---|

| 1. Find the car’s price | Usually the list price plus accessories, less qualifying employee capital contributions |

| 2. Find the appropriate percentage | Based on CO2 emissions, fuel type, and electric range rules |

| 3. Calculate the taxable benefit | Price multiplied by the appropriate percentage |

| 4. Collect employee tax | Through payroll or tax code, depending on the reporting route |

| 5. Calculate employer Class 1A NIC | Usually due on the taxable benefit after the tax year |

HMRC’s company car benefit appropriate percentage tables set out the percentages. Fully electric cars remain tax-efficient, but the percentage is rising. For 2026/27, the appropriate percentage for a zero-emission car is 4%.

For petrol, diesel, and hybrid vehicles, the percentage depends on emissions and other details. Diesel cars can carry a supplement unless they meet the relevant emissions standard. Hybrids may need the electric range figure. This is one of those areas where using an old spreadsheet can quietly produce the wrong answer.

HMRC also publishes a company car and car fuel benefit calculator. It is useful, but it does not replace clean records. The calculator still needs the correct list price, dates, emissions, fuel, and contribution figures.

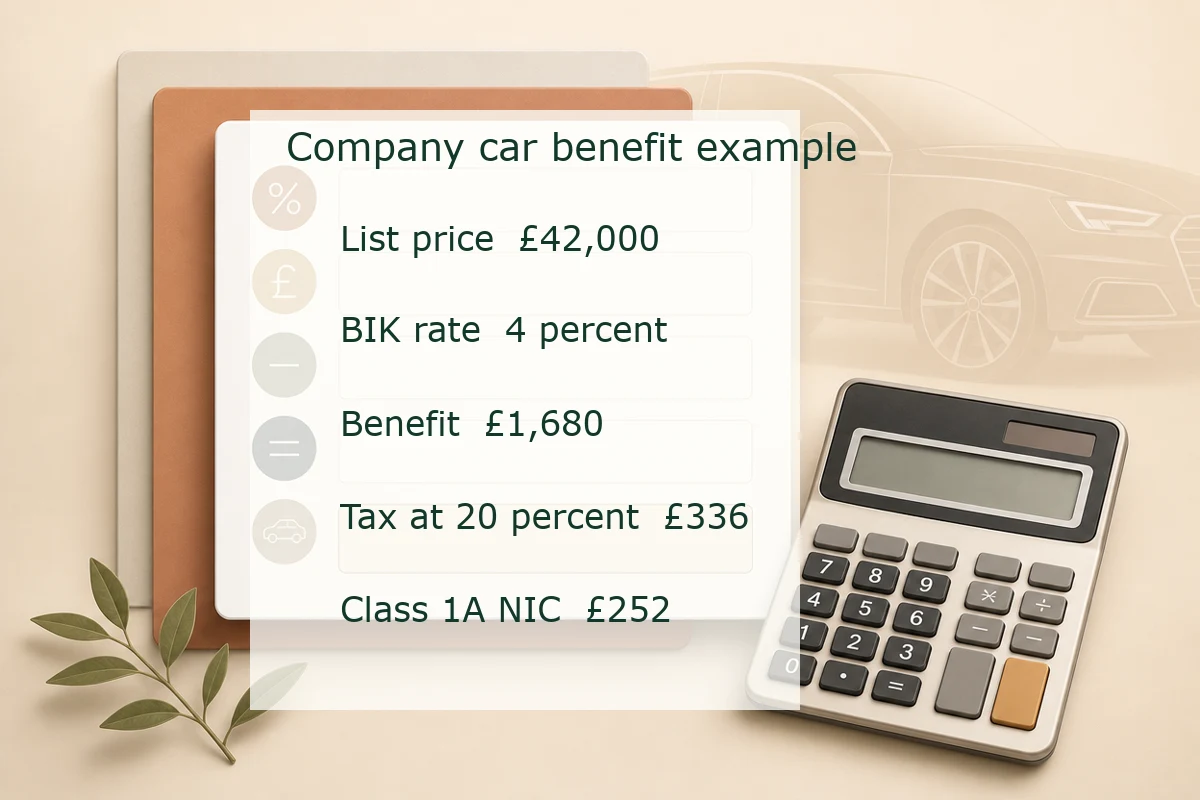

Worked example 1: electric company car in 2026/27

Assume a director has a fully electric company car available for the full 2026/27 tax year.

- list price for benefit purposes: £42,000

- appropriate percentage for a zero-emission car in 2026/27: 4%

- taxable company car benefit: £42,000 x 4% = £1,680

If the director is a basic-rate taxpayer, the personal tax cost is:

- £1,680 x 20% = £336

The employer also needs to budget for Class 1A National Insurance. Using a 15% Class 1A NIC rate:

- £1,680 x 15% = £252

So the car may feel cheap from a benefit tax point of view, but it is not nil. The employer still has a reporting and Class 1A NIC job.

Worked example 2: car provided part-way through the year

Assume the same car is first available on 1 October 2026 rather than 6 April.

The full-year benefit is still £1,680, but the car is only available for roughly half the tax year. A simple estimate is:

- full-year benefit: £1,680

- available for about 6 months out of 12

- taxable benefit estimate: £1,680 x 6 / 12 = £840

At 20% tax, the employee cost would be roughly £168. Employer Class 1A NIC at 15% would be roughly £126.

That example is simplified. Exact dates matter, and HMRC’s rules use days rather than a rough half-year split. The point is that availability dates are not admin trivia. They change the tax.

Worked example 3: private fuel can be more expensive than expected

Private fuel is a separate benefit. For 2026/27, HMRC’s published car fuel benefit multiplier is £29,200. The taxable fuel benefit is the multiplier multiplied by the same appropriate percentage used for the car.

Using the electric car above would not normally create a petrol or diesel fuel benefit. So use a petrol car with a 31% appropriate percentage.

- car fuel benefit multiplier: £29,200

- appropriate percentage: 31%

- taxable fuel benefit: £29,200 x 31% = £9,052

At 40% tax, the employee tax cost would be:

- £9,052 x 40% = £3,620.80

Employer Class 1A NIC at 15% would be:

- £9,052 x 15% = £1,357.80

That is why private fuel often needs a hard look. If the employee’s private mileage is low, reimbursing the business for all private fuel can be cheaper than carrying the fuel benefit for the year. The reimbursement rules are strict, so get advice before changing the arrangement.

Advisory fuel rates are a separate check

HMRC’s advisory fuel rates are often mixed up with company car benefit rules. They are not the same thing.

Advisory fuel rates are used when:

- an employee repays the employer for private fuel in a company car

- the employer reimburses business fuel in a company car

They are updated quarterly. The rates from 1 June 2026 apply for journeys from that date, with the usual one-month period where employers can use the previous rates after a change. The exact pence-per-mile rate depends on engine size and fuel type.

Here is the practical split:

| Question | Relevant rule |

|---|---|

| What is the taxable company car benefit? | Appropriate percentage tables |

| What is the taxable private fuel benefit? | Car fuel multiplier and appropriate percentage |

| What pence per mile can be used for company car fuel reimbursement? | Advisory fuel rates |

| What mileage can an employee claim for using their own car? | Approved mileage allowance payments, usually 55p for the first 10,000 business miles in 2026/27 |

Keep those four separate. If a director says, “I used the HMRC mileage rate,” ask which rate they mean. The wrong rate in the wrong place can create tax, NIC, or payroll corrections later.

What happens if you miss the P46(Car) deadline?

HMRC’s company car reporting page is focused on telling employers how and when to report changes. The immediate damage from a missed P46(Car) deadline is usually practical rather than a neat fixed fine.

The employee’s tax code may be wrong. PAYE may collect too little or too much tax. Payroll may not match the year-end benefit records. The P11D may need extra checking. If the car fuel position was missed, the employee could be surprised by a much larger taxable benefit later.

Here is a simple case.

An employee receives a company car on 15 June 2026. The employer forgets to report it until January 2027. The annual taxable benefit is £4,800, and the employee is a basic-rate taxpayer.

Rough tax for a full year would be:

- £4,800 x 20% = £960

If HMRC only updates the tax code late in the year, the tax collection is squeezed into fewer months or carried into a later code. The employer may also need to correct payroll records if the benefit should have been payrolled.

That is avoidable. Build a simple internal rule: no car order, lease change, fuel card, or returned vehicle is complete until payroll has been told.

A month-end company car reporting checklist

Use this at month end, especially in June, July, October, January, and April.

| Check | Why it matters |

|---|---|

| Any new company cars this month? | May trigger P46(Car) or payroll car data |

| Any returned or swapped cars? | Availability dates affect the taxable benefit |

| Any private fuel added or withdrawn? | Fuel benefit can be costly if missed |

| Any employee contributions made? | Contributions may reduce the taxable benefit if treated correctly |

| Are emissions and list price saved? | Payroll cannot calculate from a registration number alone |

| Are payrolled car benefits appearing on FPS? | HMRC needs the data if P46(Car) is not used |

| Are bookkeeping codes clear? | Motor costs, fuel, and employee repayments need review |

| Is the year-end P11D(b) Class 1A figure building correctly? | Payrolling does not remove the employer NIC job |

For a small limited company, we would usually connect this checklist to payroll processing and bookkeeping review. A car change should not sit in someone’s email inbox until year end. If you want that handled as part of a recurring process, our payroll services and bookkeeping service are the right starting points.

FAQ: P46(Car) and company car reporting

Do I need to submit a P46(Car) if the company car benefit is payrolled?

Not usually in the same way, if the car benefit is correctly payrolled and the required car data is sent through the FPS. Check the payroll setup carefully. If the car is not being reported through payroll, P46(Car) may still be needed.

Is P46(Car) the same as P11D?

No. P46(Car) tells HMRC about company car and fuel changes during the tax year. P11D is a year-end form for taxable benefits that were not payrolled. P11D(b) reports employer Class 1A National Insurance.

What is the next P46(Car) deadline after 5 July 2026?

For changes between 6 April and 5 July 2026, the online P46(Car) deadline is 2 August 2026. The next quarterly deadline after that is 2 November 2026 for changes between 6 July and 5 October 2026.

Do pool cars need P46(Car)?

Proper pool cars can be exempt from company car benefit rules, but the conditions are strict. A car is not a pool car just because several employees use it. You need evidence that it is not normally kept at an employee’s home and is not used for private journeys beyond very limited use.

Does private fuel always create a taxable benefit?

Private fuel provided for a company car can create a separate taxable fuel benefit. If the employee reimburses all private fuel using the correct method and timing, the fuel benefit may be avoided. Get the records right, because fuel benefits can be expensive.

Who should own company car reporting in a small business?

Payroll should usually own the reporting, but payroll needs data from directors, finance, HR, and whoever orders vehicles. The cleanest setup is a single company car change form or checklist that must be completed before the car is handed over.

Your next step

Open your vehicle list and check three dates: when each car became available, when private fuel started or stopped, and when payroll was told. If those dates are missing, fix that before the next quarterly deadline. It is much easier to report a car change in the right quarter than to explain a muddled tax code six months later.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

P11D Deadline 6 July 2026: UK Employer Guide to Benefits and Expenses

P11D deadline 6 July 2026 explained for UK employers, with what to report, Class 1A NIC examples, penalties, and a checklist.

PAYE Settlement Agreement Deadline 5 July 2026: Employer Guide

PAYE Settlement Agreement deadline guide for 2026, with PSA dates, eligible benefits, tax gross-up examples, and employer checklist.

ERS Return Deadline 6 July 2026: Share Scheme Guide for UK Employers

ERS return deadline 6 July 2026 explained, with EMI notifications, nil returns, penalties, share events, and employer checklist.