PAYE Settlement Agreement Deadline 5 July 2026: Employer Guide

PAYE Settlement Agreement deadline guide for 2026, with PSA dates, eligible benefits, tax gross-up examples, and employer checklist.

PAYE Settlement Agreement Deadline 5 July 2026: Employer Guide

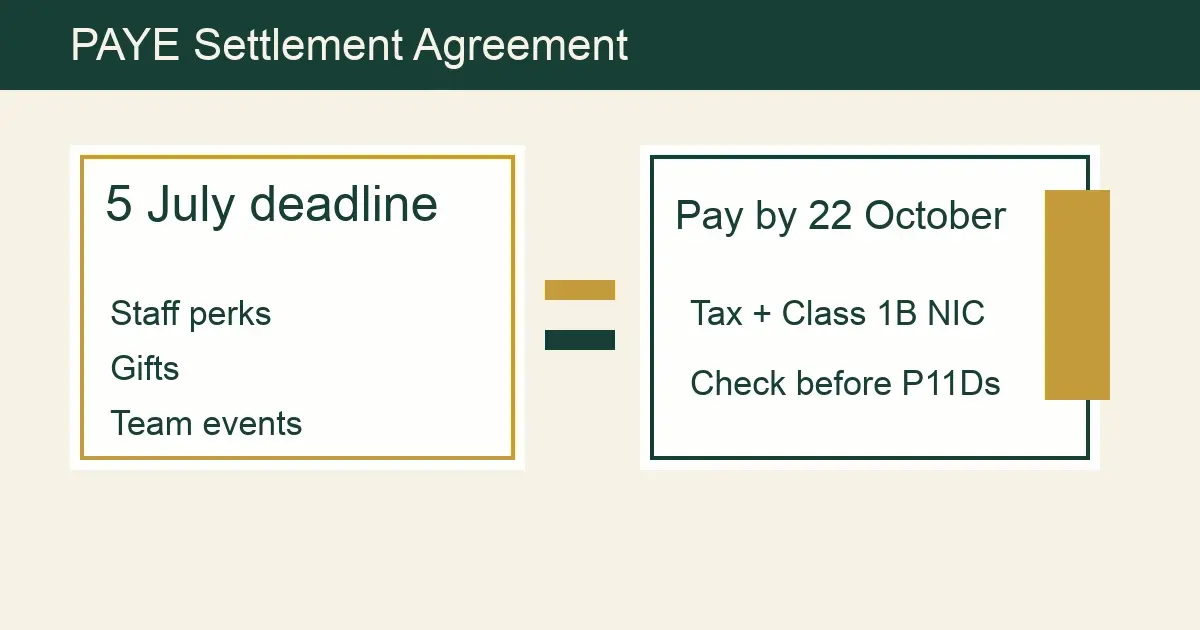

The PAYE Settlement Agreement deadline for 2025/26 expenses and benefits is 5 July 2026. If your business gave employees minor gifts, irregular perks, taxable staff entertainment, or shared benefits that are awkward to split across individual employees, a PSA can let the company pay the tax and National Insurance in one annual settlement rather than putting every item on P11Ds.

That sounds tidy, but the timing is tight. 5 July 2026 falls on a Sunday, the P11D deadline is the next day, and HMRC recommends sending the PSA calculation by 31 July 2026. The electronic payment deadline for the tax and Class 1B National Insurance is 22 October 2026, or 19 October 2026 if paying by post.

Quick summary: apply for a new PAYE Settlement Agreement by 5 July 2026 for 2025/26 items, report anything that cannot go in the PSA separately, send the calculation by 31 July 2026 where possible, and pay by 22 October 2026 electronically. The 2025/26 Class 1B NIC rate shown by HMRC is 15%.

If you want us to check employee benefits before the July deadlines, our payroll services, bookkeeping support, and contact page are the most practical starting points.

PAYE Settlement Agreement deadline dates for 2026

A PAYE Settlement Agreement, usually shortened to PSA, is an agreement with HMRC that lets an employer pay the Income Tax and National Insurance due on certain employee expenses and benefits. GOV.UK says a PSA can cover items that are minor, irregular, or impracticable. If the PSA covers the item correctly, you do not put that item through payroll, include it on the employee’s P11D, or pay Class 1A NIC on it. Instead, the employer pays the tax and Class 1B NIC under the PSA.

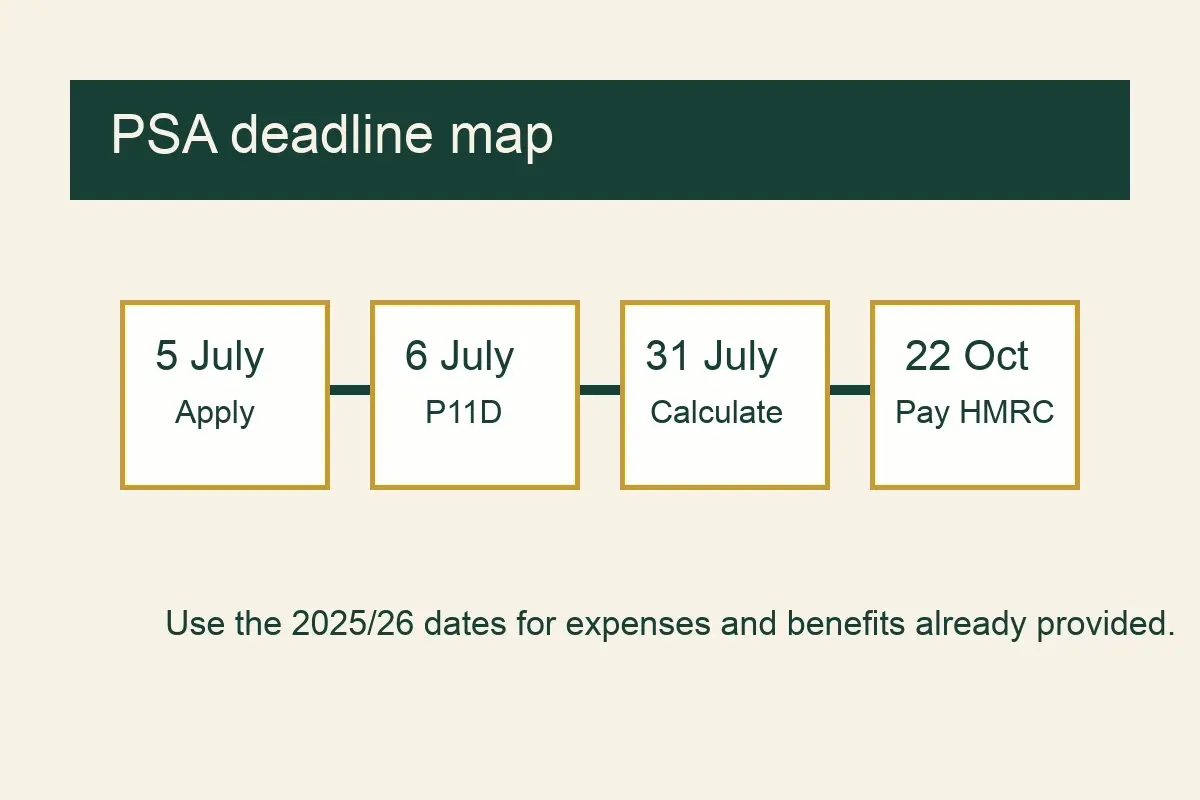

The main 2026 dates are:

| Task | Deadline for 2025/26 items | Practical point |

|---|---|---|

| Apply for a new PSA or amend the agreement | 5 July 2026 | Applies to the first tax year covered by the agreement |

| File P11Ds and P11D(b), where needed | 6 July 2026 | Items outside the PSA may still need reporting |

| Send the PSA calculation | 31 July 2026 recommended | HMRC says to send the calculation by 31 July following the tax year |

| Pay PSA tax and Class 1B NIC electronically | 22 October 2026 | Postal payment deadline is 19 October 2026 |

Official HMRC references are worth keeping open while you review the year:

- GOV.UK PAYE Settlement Agreement deadlines and payment

- GOV.UK what can be included in a PSA

- GOV.UK help with PAYE Settlement Agreement calculations

That third link is technical, but useful. It explains the records HMRC expects, the grossing-up method, and how Class 1B NIC fits into the calculation.

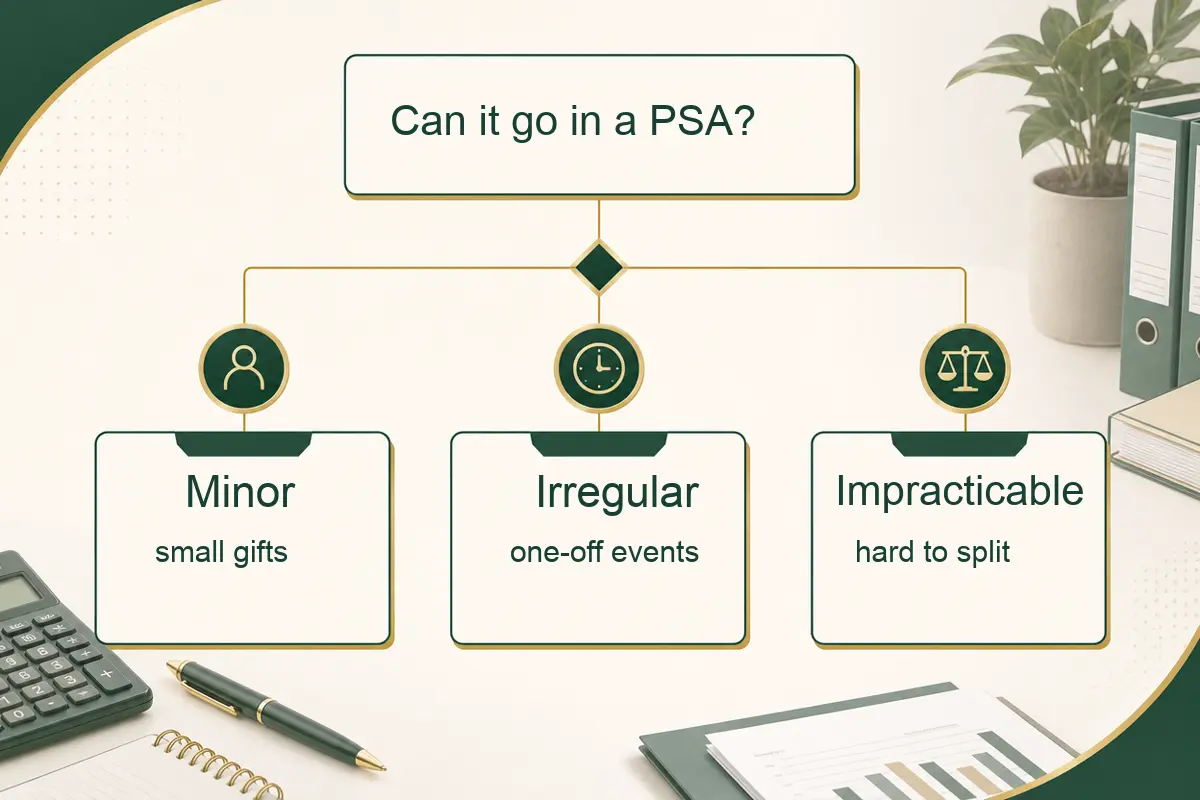

What can go in a PAYE Settlement Agreement?

HMRC splits PSA items into three groups: minor, irregular, and impracticable. An item only needs to fit one of those groups, but you should be able to explain why it fits.

| PSA category | Plain English meaning | Examples HMRC gives or commonly sees |

|---|---|---|

| Minor | Small value or incidental items | small gifts, vouchers, staff entertainment tickets, incentive awards |

| Irregular | Not paid at regular intervals and not contractual | one-off relocation cost over the exempt limit, overseas conference costs, use of a company holiday flat |

| Impracticable | Hard to value or split between employees | taxable staff entertainment, shared cars, personal care expenses |

Minor does not mean “anything below a number you like”. It means the item is small enough, in context, to be settled centrally. A £20 thank-you gift is very different from a £2,000 gift card for a director.

Irregular means the employee does not get the item as part of normal pay or a standing entitlement. A one-off staff reward after a difficult project may fit. A monthly gym payment probably does not.

Impracticable is the category that often helps with staff events. If a company pays for a taxable event where people attend in mixed numbers, bring guests, or do not all use the same amount of food, drink, or transport, it may be hard to divide the cost fairly across employees. A PSA can be cleaner than assigning tiny taxable benefits to each person.

There is a separate point about trivial benefits. If a benefit is genuinely exempt as a trivial benefit, you do not need to include it in a PSA. In broad terms, that exemption can apply where the benefit costs £50 or less, is not cash or a cash voucher, is not a reward for work or performance, and is not provided under a salary sacrifice or contractual arrangement. Directors of close companies have an annual cap for trivial benefits. The rules are narrow enough that we would still check anything close to the line.

What cannot go in a PSA?

A PSA is not a place to hide normal pay. GOV.UK says you cannot include wages, high-value benefits such as company cars, or cash payments such as employee bonuses, round sum allowances, or beneficial loans.

That matters because the wrong route can create two problems at once. The employee may still need a P11D entry or payroll treatment, while the employer may also have sent a PSA calculation that HMRC later rejects or adjusts. Nobody enjoys redoing benefits reporting in August. HMRC admin has its charms, but they are well hidden.

Here are common edge cases.

| Item | PSA treatment | Safer route if not suitable |

|---|---|---|

| Cash bonus | Not suitable | Payroll through PAYE |

| Company car | Not suitable | P11D or payrolling benefits, depending on setup |

| Director’s regular fuel benefit | Usually not suitable as a PSA item | P11D or payrolling benefits |

| Small non-cash voucher as a one-off thank-you | May be suitable if not exempt already | PSA or trivial benefit review |

| Staff event over the annual party exemption | May be suitable | PSA if agreed, otherwise P11D/payroll route |

| Round sum travel allowance | Not suitable | Payroll or expenses review |

If you apply for a PSA after the start of the tax year, HMRC also has restrictions around items already included in tax codes or PAYE deductions. For a 2025/26 PSA application made by 5 July 2026, review whether anything was already payrolled, coded out, or reported elsewhere before you assume it can be swept into the agreement.

Our P11D deadline guide explains the neighbouring P11D process. The short version is simple: do the PSA review before P11Ds are filed, not after.

How the PSA tax gross-up works

The part that surprises employers is the gross-up. A PSA means the employer pays the employee’s tax on the benefit. Paying that tax for the employee is itself treated as a further benefit, so HMRC uses a grossed-up tax calculation.

HMRC’s basic method is:

- Multiply the value of the benefit by the employee’s tax rate.

- Multiply that answer by 100.

- Divide by 100 minus the employee’s tax rate.

You repeat that for each employee tax-rate group, such as basic-rate, higher-rate, additional-rate, and Scottish rates where relevant.

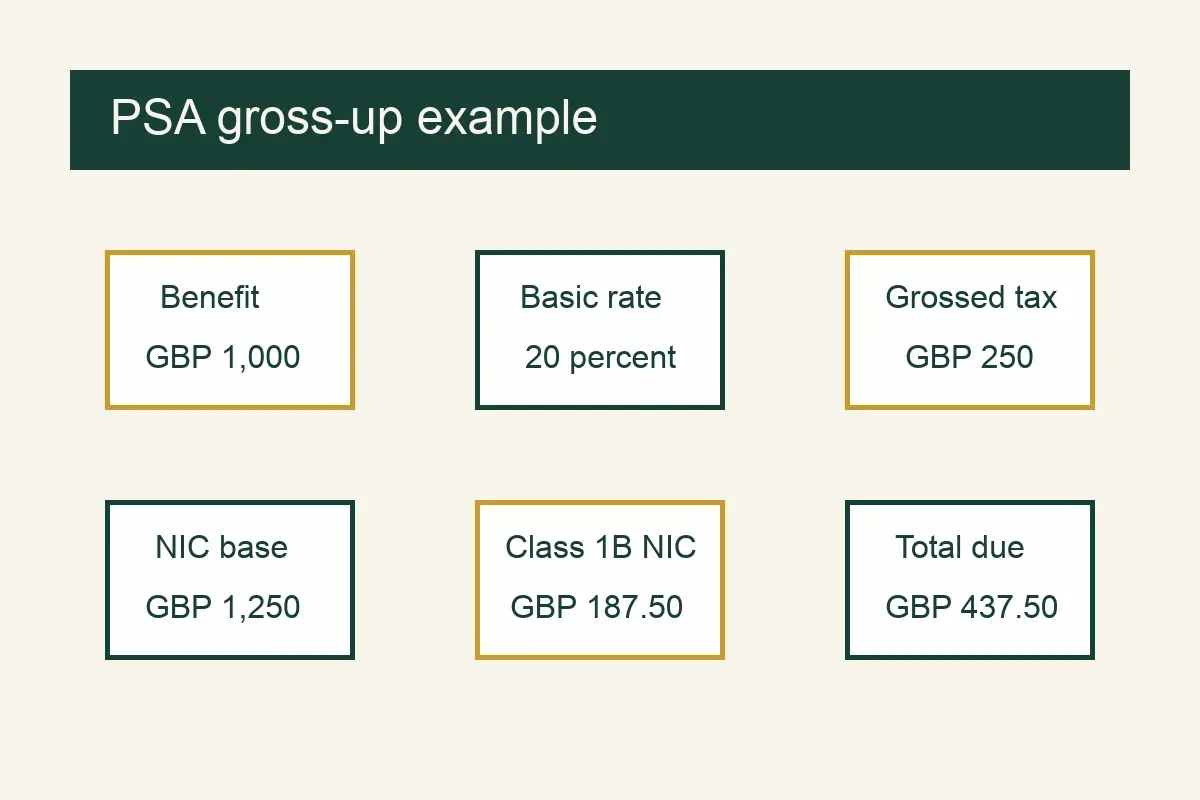

Worked example 1: £1,000 benefit for a basic-rate employee

Assume an English employee receives a PSA item worth £1,000 and the right rate for the calculation is 20%.

| Step | Calculation | Amount |

|---|---|---|

| Benefit value | Given | £1,000 |

| Tax at 20% | £1,000 × 20% | £200 |

| Grossed-up tax | £200 × 100 ÷ 80 | £250 |

| Class 1B NIC base | £1,000 + £250 | £1,250 |

| Class 1B NIC at 15% | £1,250 × 15% | £187.50 |

| Total PSA payment | £250 + £187.50 | £437.50 |

The employee got a benefit worth £1,000. The employer’s PSA tax and NIC cost is £437.50, so the total employer cost is £1,437.50 before any VAT or accounting adjustments.

Worked example 2: same type of gift, higher-rate employee

Now assume a higher-rate employee receives taxable non-cash gifts with a PSA value of £600. The right tax rate for that employee is 40%.

| Step | Calculation | Amount |

|---|---|---|

| Benefit value | Given | £600 |

| Tax at 40% | £600 × 40% | £240 |

| Grossed-up tax | £240 × 100 ÷ 60 | £400 |

| Class 1B NIC base | £600 + £400 | £1,000 |

| Class 1B NIC at 15% | £1,000 × 15% | £150 |

| Total PSA payment | £400 + £150 | £550 |

That is why PSAs need budgeting. The higher the employee’s tax rate, the more expensive it is for the employer to settle the tax for them.

Worked example 3: staff entertainment and the annual party limit

Staff entertainment is one of the most common PSA review areas. The annual party exemption can cover annual events where the cost is £150 or less per head, the event is open to all employees, and the other conditions are met. It is an exemption, not an allowance. Go over the limit for an event and that event may become taxable in full.

Assume a company has 10 employees and runs two events in 2025/26:

| Event | Total cost | Cost per head |

|---|---|---|

| Summer meal | £800 | £80 |

| Winter party | £1,850 | £185 |

The company can choose the event, or combination of events, that best uses the exemption, as long as the conditions are met. Here, the summer meal at £80 per head can be exempt. The winter party at £185 per head is above the £150 limit, so it cannot be partly exempt under that rule. The full winter party cost may need tax treatment.

If the winter party is included in a PSA and all 10 employees are basic-rate taxpayers, the rough calculation looks like this:

| Step | Calculation | Amount |

|---|---|---|

| Taxable event cost | Given | £1,850 |

| Tax at 20% | £1,850 × 20% | £370 |

| Grossed-up tax | £370 × 100 ÷ 80 | £462.50 |

| Class 1B NIC base | £1,850 + £462.50 | £2,312.50 |

| Class 1B NIC at 15% | £2,312.50 × 15% | £346.88 |

| Total PSA payment | £462.50 + £346.88 | £809.38 |

Your exact answer may differ if some employees are higher-rate taxpayers, Scottish taxpayers, directors, guests, or non-employees. It is still a useful illustration. A “small” overspend on an event can turn into a meaningful employer tax cost.

Records to gather before you apply

PSA work is much easier when the payroll, bookkeeping, and expense records agree with each other. Before applying, gather:

- staff gift and voucher records

- staff event invoices and attendee lists

- expense claims that include non-business elements

- travel and subsistence records where daily limits were exceeded

- any relocation expenses over the exempt amount

- employee tax-rate information for the calculation

- details of items already payrolled, coded out, or reported on P11Ds

- notes explaining why each PSA item is minor, irregular, or impracticable

HMRC’s calculation guidance says employers should keep enough detail to support the value of the benefits, the number of employees, the relevant employee tax rates, the grossed-up tax, and the Class 1B NIC. It also says employers must keep PSA agreement records for at least 3 years after the end of the most recent tax year they relate to.

That is more than a receipt folder. For example, a restaurant invoice tells you what was spent, but it may not tell you whether employees, spouses, clients, or contractors attended. A gift-card invoice tells you the total order value, but it may not tell you which employees received cards and whether any director trivial-benefit cap is affected.

Good bookkeeping helps here. If staff welfare, client entertaining, travel, gifts, and payroll costs are all posted to vague account codes, the PSA review becomes slower and more expensive. Clear categories save time in July.

How to apply for a PAYE Settlement Agreement

You can apply to HMRC online for a new PSA, or to change or cancel an existing one. The application needs employer details and the type of expenses or benefits you want the agreement to cover.

Use specific descriptions. “Staff benefits” is too vague. “Taxable staff entertainment where individual allocation is impracticable” is much more useful. “Minor non-cash gifts and vouchers not covered by the trivial benefits exemption” is clearer than “gifts”.

Once HMRC has the agreement in place, you still need to tell HMRC what you owe each year. A PSA is not a one-time payment instruction. It is an agreement covering the treatment of the items, followed by an annual calculation and payment.

If HMRC calculates the amount because you did not submit the calculation, GOV.UK warns you may be charged more. That is a good reason to send the calculation promptly, even where the amount is nil.

Common PSA mistakes small employers make

The first mistake is using a PSA for items that should have gone through payroll. Cash bonuses, allowances, and normal earnings are PAYE items. A PSA will not make them minor just because the employer would prefer one annual bill.

The second mistake is missing the P11D interaction. An item outside the PSA may still need to be reported on a P11D by 6 July 2026. If you discover that after the P11D deadline, you may be into corrections, late filing risks, or awkward employee conversations.

The third mistake is ignoring tax-rate groups. A calculation using 20% for everyone may understate the PSA bill if some employees are higher-rate, additional-rate, or Scottish taxpayers. HMRC expects separate calculations for groups with different rates.

The fourth mistake is forgetting Class 1B NIC on the tax itself. Class 1B NIC is not just charged on the original benefit value. HMRC’s guidance says it is due on the value of items that would normally attract Class 1 or Class 1A liability and on the total tax payable under the agreement.

The fifth mistake is treating a staff party as automatically exempt. The £150 per head annual event rule is helpful, but it has conditions. It is not a general entertaining allowance.

A practical employer checklist for June and early July

Use this checklist before 5 July 2026:

- list all 2025/26 gifts, vouchers, staff events, travel extras, and unusual perks

- remove items that are clearly exempt, such as genuine trivial benefits or qualifying annual events

- remove items that clearly cannot go in a PSA, such as cash bonuses and company cars

- group the remaining items as minor, irregular, or impracticable

- check whether any item has already been payrolled or included in a tax code

- decide what must be reported on P11D or P11D(b)

- apply for or amend the PSA by 5 July 2026

- send the PSA calculation by 31 July 2026 where possible

- schedule the electronic payment for 22 October 2026

For a small employer, the best time to do this is late June, when the payroll year-end is fresh and before the P11D deadline becomes urgent. If the records are messy, start with the bank account and bookkeeping codes, then work back to invoices and attendees.

When to get help

A straightforward PSA for a few staff gifts can be manageable. A PSA involving directors, mixed tax-rate groups, overseas employees, Scottish taxpayers, relocation costs, or several staff events deserves a proper check.

The risk is not only the tax amount. It is also reporting the same item twice, missing a P11D item, using the wrong tax rate, or including something HMRC later says was never suitable for a PSA.

If your business gave staff perks during 2025/26, set aside one hour before 5 July 2026 to sort them into four piles: exempt, payroll, P11D, and PSA. That one exercise will usually tell you whether you can handle the filing internally or whether it is time to ask us to review it through payroll support or contact us before the July deadlines land.

PAYE Settlement Agreement FAQs

What is a PAYE Settlement Agreement?

A PAYE Settlement Agreement is an agreement with HMRC that lets an employer pay the tax and National Insurance on certain minor, irregular, or impracticable employee expenses and benefits in one annual settlement.

What is the PAYE Settlement Agreement deadline for 2025/26?

For the 2025/26 tax year, the application deadline is 5 July 2026. HMRC recommends sending the calculation by 31 July 2026. The electronic payment deadline is 22 October 2026, with 19 October 2026 applying for postal payment.

Do employees pay tax on PSA items?

The employee is the person whose tax liability is being settled, but the employer pays that tax under the PSA. Because the employer pays the employee’s tax, the calculation is grossed up.

Does a PSA replace P11D forms?

Only for items correctly covered by the PSA. Items outside the PSA may still need P11D reporting by 6 July 2026, or payroll treatment if they should have gone through PAYE.

What is the Class 1B NIC rate for 2025/26 PSAs?

HMRC’s PSA calculation guidance lists the 2025/26 Class 1B NIC rate as 15%. Class 1B NIC is paid by the employer and does not give employees benefit entitlement.

Can directors use a PSA?

Directors can be included where the item is genuinely suitable for a PSA, but director benefits often need closer checking. Close company directors also have special trivial-benefit cap rules, so do not assume all small director perks can be ignored.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

1257L M1 Tax Code Explained: Emergency Tax Guide for 2026/27

1257L M1 tax code explained for 2026/27, with emergency tax calculations, refund examples, and practical steps to correct your code.

P46 Car Form Deadline 2026/27: Company Car Reporting Guide

P46 Car form deadline 2026/27 explained for employers, with quarterly dates, payroll rules, company car tax examples, and checks.

ERS Return Deadline 6 July 2026: Share Scheme Guide for UK Employers

ERS return deadline 6 July 2026 explained, with EMI notifications, nil returns, penalties, share events, and employer checklist.