How Tips Are Taxed in the UK: Income Tax & NI Explained

Learn how tipping is taxed in the UK, who pays the tax, and how it affects your income tax and National Insurance. A must-read for hospitality and service staff.

How To Tax Tipping: Effects on Income Tax & National Insurance

How Tips are Paid

Tips can be paid directly in cash at the end of a shift or accumulated and distributed among all employees. Regardless of the method, tips do not count towards the national minimum wage. However, they are subject to income tax. If tips are paid directly by customers, only income tax is applicable, not National Insurance. Conversely, if tips are distributed by the employer, both income tax and National Insurance must be paid.

Tax Obligations

Income tax must be paid on any tips received, and sometimes National Insurance deductions are also applicable. If you are filing an income tax return, you must include your tips. If not, HMRC will assess your tips based on the information provided by you or your employer. Additionally, responsibility for paying income tax depends on how the tips are distributed. If the employer pays directly, they handle the tax through the PAYE system. If tips are pooled and distributed by a “troncmaster,” the troncmaster is responsible for the tax.

Service Charges and Bonuses

Service charges, if mandatory, are not considered tips and are processed as regular pay. Voluntary service charges are treated like tips for tax purposes. Bonuses, on the other hand, are part of your salary and are subject to both income tax and National Insurance through PAYE.

Impact on Income Tax

The impact of tips on income tax depends largely on how they are managed and reported. Employees receiving direct tips must report these amounts accurately to ensure correct tax calculations. Misreporting can lead to underpayment or overpayment of taxes, resulting in potential penalties or refunds. Proper documentation and transparency with HMRC are essential for compliance.

National Insurance Contributions

National Insurance contributions for tips are only applicable under certain conditions. When an employer is involved in distributing tips, these payments are treated as additional earnings, attracting National Insurance. Direct tips from customers bypass this, focusing solely on income tax. Employees must understand these nuances to avoid unexpected deductions and ensure accurate contributions.

Bonuses and Taxation

Bonuses are an integral part of an employee’s remuneration and are subject to both income tax and National Insurance through the PAYE system. Unlike tips, which may vary in how they are taxed based on how they are distributed, bonuses are always treated as standard earnings. This means they are added to the employee’s gross income and taxed at the appropriate rate, ensuring that both income tax and National Insurance contributions are accurately calculated and deducted by the employer. This consistent treatment simplifies compliance for both employees and employers.

Understanding the tax implications of tips is essential for ensuring compliance and avoiding unexpected tax liabilities. Both employees and employers must be aware of their responsibilities to handle tips correctly within the legal framework.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

Sole Trader Guide UK: Responsibilities, Setup & Self-Employment Explained

Thinking of becoming a sole trader? Learn what self-employment involves, your responsibilities, and how sole traders differ from LTDs or partnerships in the UK.

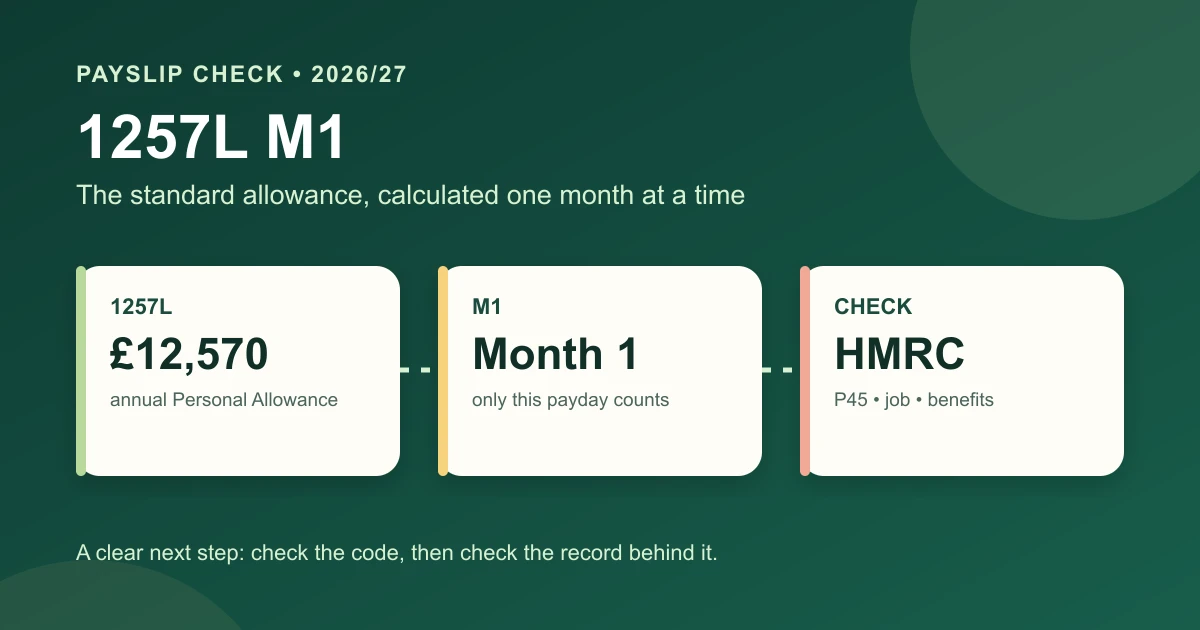

Tax Code 1257L M1 Explained: What It Means for Your Pay in 2026/27

Tax code 1257L M1 explained for 2026/27, including emergency tax, monthly allowances, payslip examples and how to fix it.

Director's Loan Tax 2026: Section 455, the £10,000 Rule and 9-Month Deadline

Director's loan tax 2026 explained: Section 455 at 33.75%, the £10,000 benefit rule, repayment timing and worked examples.